In an AL3 file, the 5LAG (Location Address Group) and 5SLC (Sub-Location Group) play very important roles in representing how property or risk locations are structured within a commercial insurance policy — especially for lines like Commercial Property, BOP (Business Owners Policy), Inland Marine, and Farm policies.

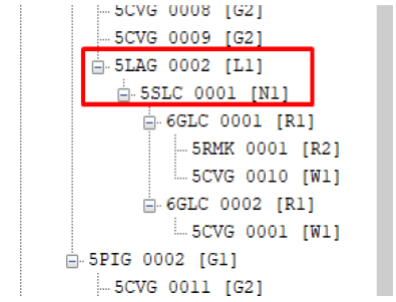

Typical hierarchy example:

5LAG — Location Address Group

5LAG is used to define each insured location’s address details within the policy.

It identifies where the risk is located — such as a building, premises, or insured location.

Contains information like:

- Street address

- City

- State/Province

- ZIP/Postal Code

- County or Fire District

Importance:

- Identifies the risk location — crucial for underwriting, rating, and inspection.

- Determines premium factors — e.g., fire protection class, territory rating, flood zone.

- Links coverage and sublocations — many coverages (5CVG) or buildings (5SLC) attach under a specific 5LAG.

- Regulatory & compliance requirement — insurers must report accurate risk addresses.

5SLC — Sublocation Group

Purpose:

5SLC represents a sub-location within a location — such as a building, unit, or structure on the same premises.

It allows insurers to record multiple buildings or risk items under one main location (5LAG).

Contains information like:

- Sublocation Description

- Sublocation Number

- Sublocation Type Code

- Number of Mortgagees

- Street address

- City

- State/Province

- ZIP/Postal Code

- County or Fire District

Importance:

- Allows multiple buildings under one location (e.g., Building A, B, and C on one property).

- Supports accurate coverage linkage — each 5SLC can have its own coverages (5CVG), additional interests, and remarks.

- Provides detail for risk evaluation — construction, occupancy, protection, and exposure (COPE) data are tied here.

- Improves data structure consistency — avoids redundancy and makes AL3 more modular.

Leave A Comment