Introduction to Insurance and Classes of Insurance

Insurance policy is a contract in the form of a policy that binds one party to cover the risks in exchange for time-bound premiums decided preemptively. The insurance companies generally pool the money collected from its customers and make profits on the probability that the claims made against premiums submitted would be always lesser. In this way, the insurance companies work on the principle of charging more premiums than the possibility of the claims made against it.

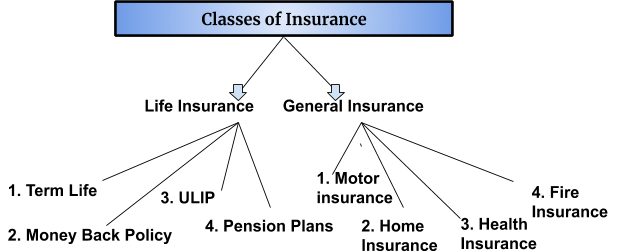

Having discussed what an insurance company is and how they make profits, we will be discussing what are the different classes of insurance companies and what exactly they are entitled to insure. The figure below charts out how the insurance industry is mainly divided into two broad categories and there are specialized fields under which the companies provide policies according to the specific fields.

General Insurance:

General insurance is referred to as a contract among parties that offer financial compensation on any damage other than death. Simply put, General insurance insures everything apart from life. It could be disabilities or any other liability related to one’s house, car, health, travel or automobile among various other things.

For example, if one has bought medical insurance and pays regular premiums to the insurer. Let’s assume that he/she falls sick and gets admitted to a hospital. Now, depending on the type of policy bought, the insurance will cover the full or partial reimbursement of the expenses. Out of the classes of insurance, this is commonly known as, Health insurance and will come under the broad category of General Insurance. However, more than health, General insurance varyingly includes Automobile, House, Fire or Travel insurance. Hence, it is implied that if someone’s car gets stolen or house sets on fire, the amount of reimbursement he/she gets would be the result of buying a General Insurance policy.

General insurance goes to the extent of including Fidelity insurance. In this kind of insurance, if someone owes money to a third party and is unable to repay due to an unforeseen circumstance, the insurance company will be obliged to pay that money to the third party.

Life Insurance:

As the name clears it out, life insurance is a contract that offers financial compensation in case of death of the insured person or disability that hinders the normal functioning of anyone. The disability term is subjective and varies from different policies. This type of insurance puts one’s family at safety, should anything happen to the breadwinner of the family. However, as shown in the above figure, there can be different subtypes of Life insurance that may include the below-listed things:

Term Insurance: It covers the insuree for a specific period and the family of the deceased gets a lump-sum pre-decided amount in the case of death. However, if the person survives the accident, no money will be given.

Whole Life Insurance: It covers the insuree for a lifetime and the family receives a certain amount of money in the case of death. The insurance company is also obliged to give a bonus on such amount as accrued based on the time of the policy.

Endowment Policy: It’s like a term policy, valid for a certain period of time and the amount goes to the family in case of death. However, in this one, the insuree is also entitled to get maturity proceeds after the term has ended.

Money back Policy: In this, a certain percentage of the sum assured is paid to the term as survival benefit. Post expiry of the term, the insuree gets the balance amount as maturity proceeds. The family gets the entire sum in case of death during the policy period and this would be regardless of the survival benefit payments made.

Unit-Linked Insurance Plans (ULIPs): These are the investment tools that double up the earnings. In this plan, a part of the premium goes towards the insurance cover and the remaining amount is invested in Debt and Equity.

Apart from the above-listed categories, Child Plans and Pension Plans also come under the Life Insurance category.

Leave A Comment